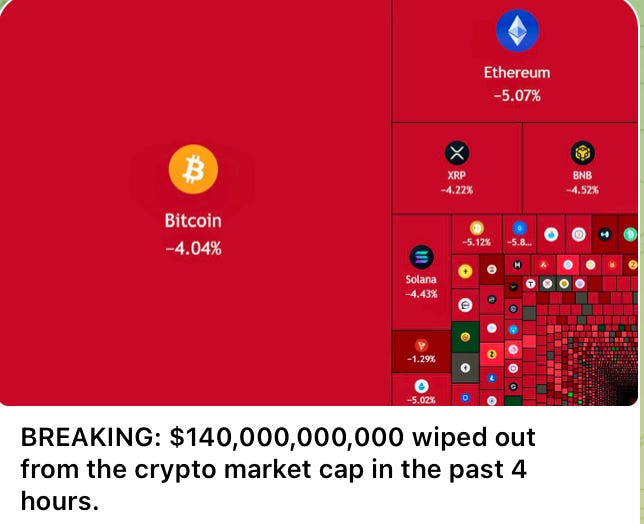

SILVER BREAKS OUT: CRYPTO SELL-OFF

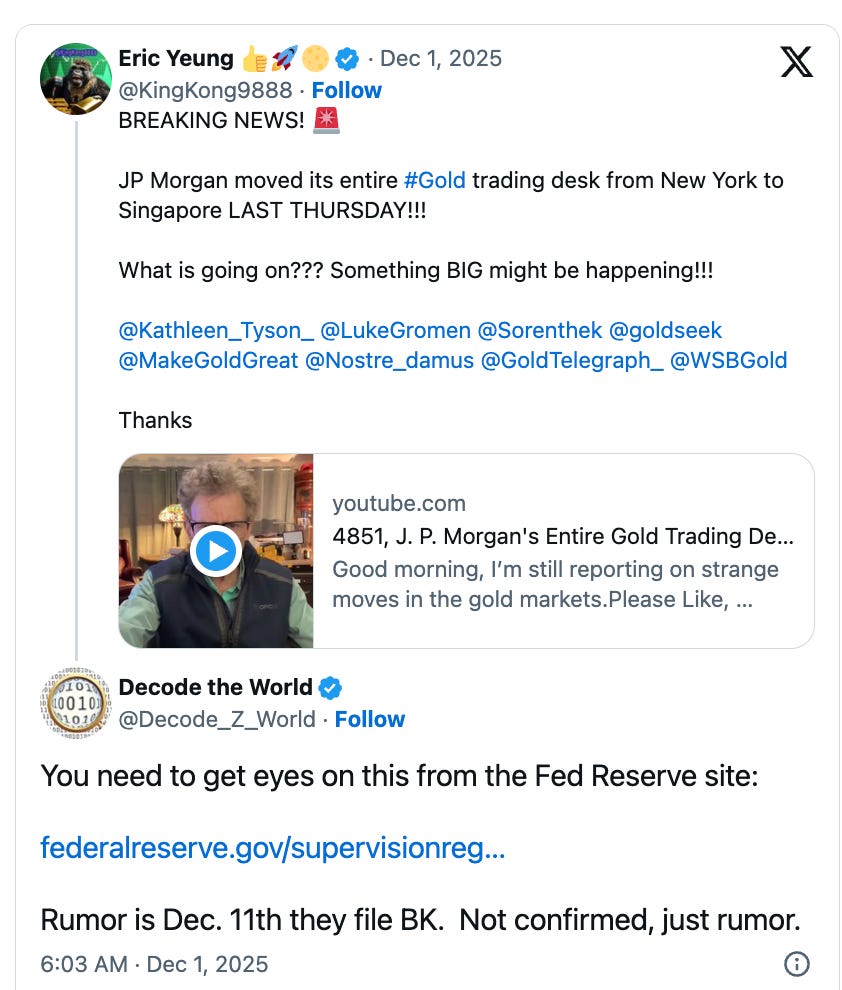

REPORT: JP Morgan/Chase Moved Entire Precious Metals Trading Staff to Singapore During Thanksgiving Holiday

Silver, at $NZ101 is up 19.6%

Meanwhile..

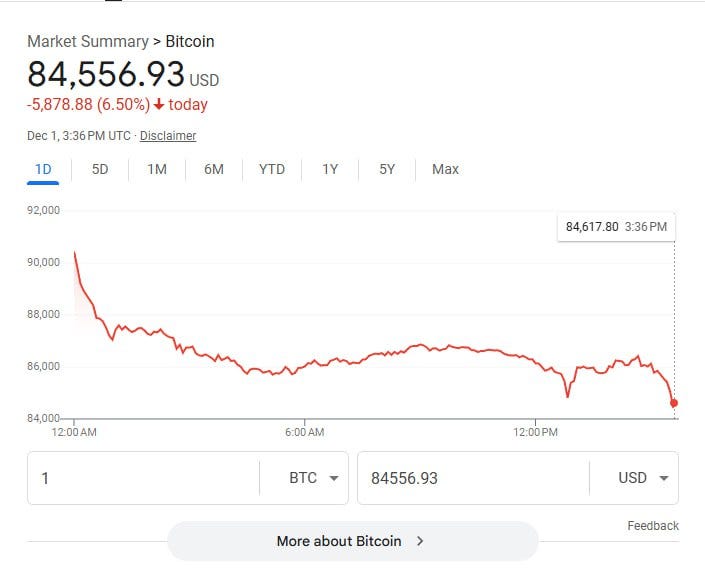

https://www.cnbc.com/2025/12/01/bitcoin-ethereum-fall-sharply-as-crypto-sell-off-resumes-.html?s=09

The Argentum Inflection: How Five Years of Structural Deficit Broke the Silver Market

Nov 29, 2025

An Institutional Analysis of the Terminal Phase in Precious Metals

By Shanaka Anslem Perera

The silver market crossed a threshold on November 28, 2025 that most institutional analysts failed to anticipate. When spot prices breached $56.72 per ounce—surpassing the October high of $54.47 and establishing a new nominal record—the move was not merely technical. It was the mathematical consequence of a supply-demand imbalance that has been compounding for half a decade, now intersecting with a regulatory reclassification that transforms silver from commodity to strategic asset.

The day’s events provided an unintended natural experiment. A cooling system failure at a CyrusOne data center in Aurora, Illinois forced the Chicago Mercantile Exchange to halt trading across its Globex platform for approximately ten hours. During this period, with the world’s largest derivatives exchange dark, silver contracts on the Shanghai Gold Exchange surged to fresh yuan highs at ¥12,682 per kilogram. When Comex reopened at 8:30 a.m. Eastern Time, spot silver immediately gapped higher, ultimately closing with a 5.53 percent daily gain—the strongest single-session advance in over a year.

This sequence illuminates a structural reality that paper markets have obscured: the physical clearing price of silver now exceeds the managed futures price by a material margin. The CME outage removed, however briefly, the dampening mechanism of infinite paper leverage. What remained was raw physical demand meeting constrained physical supply. The result was price discovery at a level the derivatives complex had previously suppressed.

The Arithmetic of Depletion

The Silver Institute, in partnership with Metals Focus, released its interim 2025 market assessment on November 13, confirming what the price action now reflects. The global silver market will record its fifth consecutive structural deficit in 2025, estimated at 95 million ounces. This follows deficits of 253 million ounces in 2022, 199 million ounces in 2023, and 149 million ounces in 2024. The cumulative shortfall from 2021 through 2025 approaches 820 million ounces—equivalent to nearly one full year of global mine production.

To grasp the magnitude of this depletion, consider the baseline. Global mine output in 2024 reached 819.7 million ounces, a modest 0.9 percent increase from the prior year. Even with recycling contributing an additional 193.9 million ounces—a twelve-year high—total supply of approximately 1.015 billion ounces failed to meet demand of 1.164 billion ounces. The market consumed 149 million ounces more than it produced.

This is not a transient imbalance. The deficit persists because approximately 70 percent of silver production emerges as a byproduct of copper, lead, zinc, and gold mining. A copper producer will not expand output to capture elevated silver prices if the copper market is soft. The supply response function is fundamentally broken. Primary silver mines represent only 28 percent of global output, and the lead time from discovery to production spans 10 to 15 years. The price signal has been screaming for two years; the supply response remains inaudible.

Industrial fabrication demand reached a record 680.5 million ounces in 2024, the fourth consecutive annual record. The photovoltaic sector alone consumed approximately 198 million ounces, driven by China’s installation of a staggering 278 gigawatts of solar capacity in a single year. Electric vehicles, which require roughly 50 grams of silver per unit compared to 25 grams for internal combustion engines, represent an additive demand vector that did not exist at meaningful scale five years ago.

The 2025 interim data reveals a nuanced picture. Total demand is projected to decline 4 percent to 1.12 billion ounces, with industrial fabrication easing 2 percent to 665 million ounces. This contraction reflects aggressive thrifting by solar panel manufacturers—reducing silver content per module—combined with tariff-induced economic uncertainty. Yet even with demand destruction, the deficit persists. The market cannot balance because supply cannot respond.

The Critical Mineral Designation

On November 7, 2025, the United States Geological Survey published the Final 2025 List of Critical Minerals, adding silver alongside copper, potash, silicon, rhenium, and lead. This designation, mandated by the Energy Act of 2020, identifies minerals essential to economic and national security that face supply chain vulnerabilities.

The implications extend beyond symbolism. Critical mineral status activates Title III of the Defense Production Act, empowering the executive branch to direct capital toward domestic production, streamline permitting for mining projects, and authorize strategic stockpiling. The National Defense Stockpile, which liquidated its silver holdings through the 1990s, could be mandated to rebuild reserves in a market already experiencing 95 million ounces of annual deficit.

The USGS methodology explicitly cited import dependence as a determining factor. The United States imports between 67 and 80 percent of its silver consumption annually, with Mexico as the dominant supplier. The vulnerability is acute: a trade disruption, tariff escalation, or geopolitical shock could sever access to a metal now deemed essential for photovoltaic cells, electronics, and defense applications including silver-zinc batteries in naval torpedoes.

Market participants have begun to price this regulatory shift. The fear of Section 232 tariffs—the same mechanism applied to aluminum and steel—has triggered precautionary inventory accumulation within the United States. Approximately 75 million ounces have flowed into Comex vaults since early October, yet this metal remains sequestered rather than available for global arbitrage. The critical mineral designation has introduced a new variable: price-insensitive strategic demand competing with price-sensitive industrial consumption.

The Liquidity Fracture

The events of November 28 exposed a fracture in the global arbitrage mechanism that has historically maintained price convergence across London, New York, and Shanghai. Under normal conditions, metal flows seamlessly from surplus regions to deficit regions, flattening price discrepancies within hours. The current market exhibits the opposite dynamic: regional premiums are expanding, indicating that absolute scarcity is preventing arbitrage.

London vaults, which store the physical metal backing a significant share of global exchange-traded products, face persistent tightness. The Silver Institute noted that roughly half of silver-backed ETPs are held in London, contributing to October’s liquidity squeeze that drove lease rates to extraordinary levels. When investors buy shares in a silver ETF, the fund must source physical bars to allocate to the trust. In a deficit market, the ETF competes directly with Apple, Tesla, and JA Solar for 1,000-ounce bars. This competition is resolving through price—the only mechanism capable of rationing scarce supply.

Shanghai’s emergence as the price-setting venue represents a structural shift in market architecture. For decades, London and New York established the benchmark, with Asian consumers as price takers. The November 28 sequence inverted this relationship. During the Comex blackout, Shanghai silver contracts set the global price based on physical demand, and Western markets were forced to arbitrage upward upon reopening. The yuan reached 14-month highs against the dollar on the same day, amplifying the purchasing power of Chinese industrial consumers.

The gold-silver ratio, a metric tracked by precious metals investors for over a century, has compressed from above 100 in early 2025 to approximately 74 at current prices. With gold trading near $4,200 per ounce, the historical mean of 60 would imply silver at $70. The ratio’s compression during precious metals bull markets has historically been violent and extended. In 1980, the ratio collapsed to 17; in 2011, it reached 32. The current reading suggests silver retains significant relative value against its monetary cousin.

The Thermodynamic Limit of Thrifting

A persistent bearish argument holds that elevated prices will trigger substitution and thrifting, reducing silver intensity per unit of industrial output. The 2024-2025 data refutes the efficacy of this mechanism in reversing aggregate demand growth.

Photovoltaic manufacturers have indeed reduced silver content per module through technological innovation. The industry is transitioning from PERC (Passivated Emitter and Rear Cell) technology to TOPCon (Tunnel Oxide Passivated Contact) and HJT (Heterojunction) architectures. Yet this transition presents a paradox: TOPCon cells use approximately 1.5 times more silver per gigawatt than PERC, and HJT cells use twice as much. The shift toward higher-efficiency panels increases, rather than decreases, silver intensity.

More fundamentally, efficiency gains are encountering Jevons Paradox. As thrifting reduces the silver cost per panel, solar installations become more economically viable, accelerating deployment. China installed 278 gigawatts in 2024; global installations are projected to set another record in 2025. The absolute volume of panels overwhelms the per-unit savings. Total photovoltaic silver demand is forecast to ease approximately 5 percent in 2025—but only because manufacturers have exhausted the easy efficiency gains while installation volumes continue to surge.

Silver possesses the highest electrical conductivity of any element. There exists a physical floor below which efficiency collapses. Substitution with copper or aluminum incurs performance penalties that high-efficiency panels cannot absorb. The thermodynamic properties that make silver irreplaceable in photovoltaics, electronics, and medical applications also make it inelastic to price signals. Industrial consumers cannot simply switch suppliers; they must bid for a finite, depleting resource.

The Investment Surge

Exchange-traded product flows have undergone a phase transition. After years of outflows, silver-backed ETPs recorded inflows of 187 million ounces through November 6, 2025—an 18 percent increase in holdings. This represents the strongest annual inflow since 2020 and the pandemic-era flight to hard assets.

The Silver Institute attributes this capital rotation to concerns over stagflation, Federal Reserve independence, government debt sustainability, and the dollar’s role as a reserve currency. These are not transient anxieties. The U.S. federal debt exceeds $36 trillion; the fiscal deficit for 2025 approaches $2 trillion. Central banks globally have been net buyers of gold for seven consecutive years, accumulating over 1,000 tonnes annually in 2023 and 2024. Silver, as the more volatile and industrially-leveraged precious metal, attracts capital seeking convexity to monetary debasement.

The mechanics of ETP accumulation compound the physical shortage. When BlackRock’s iShares Silver Trust acquires bars for its London vaults, that metal is removed from the available float. It cannot simultaneously back an ETF share and be consumed by a solar manufacturer. The 187 million ounces absorbed by ETPs in 2025 exceeds the annual deficit itself. Investment demand is not merely participating in the shortage; it is amplifying it.

Retail physical demand presents a more nuanced picture. Coin and bar sales in Western markets declined in 2024, with U.S. demand falling 40 percent as long-term holders took profits at elevated prices. Yet this liquidation was absorbed entirely by Indian buyers, who increased accumulation following a cut in import duties, and by the institutional ETP complex. The net effect was a continued deficit. The marginal seller found a marginal buyer at progressively higher prices.

The Geopolitical Calculus

Silver’s reclassification as a critical mineral occurs within a broader context of resource nationalism and supply chain securitization. The United States, European Union, and China are engaged in a competition for materials deemed essential to the energy transition and advanced manufacturing. Lithium, cobalt, rare earths, and copper have dominated policy attention. Silver’s addition to this list signals recognition that the energy transition cannot proceed without securing supply chains for photovoltaic metallization.

Mexico, the world’s largest silver producer, accounts for approximately 24 percent of global mine output. Any escalation in U.S.-Mexico trade relations—tariffs, border disputes, regulatory friction—introduces supply risk that cannot be quickly offset. Peru, the second-largest producer, faces chronic political instability that has intermittently disrupted mining operations. Bolivia, with significant undeveloped deposits, operates under a nationalist resource policy that limits foreign investment.

Russia announced in late 2025 an intention to purchase $535 million in silver over three years for strategic reserves—the first major central bank silver accumulation since the commodity’s demonetization decades ago. If this precedent triggers competitive accumulation by other central banks, particularly China and India, the demand shock would dwarf current deficits. Central bank gold purchases removed approximately 1,000 tonnes annually from private markets; equivalent silver accumulation would represent approximately 350 million ounces—more than three times the current annual deficit.

The Price Discovery Regime

The market has entered a phase that technical analysts describe as price discovery mode. The breach of $54.47 eliminated the final overhead resistance from the 45-year consolidation below the 1980 and 2011 peaks. Silver now trades in a zone with no historical reference points for resistance—only air.

Metals Focus, the research firm behind the Silver Institute’s annual survey, projects silver prices reaching $60 per ounce by 2026. UBS has lifted its target to a similar level. These forecasts, while constructive, may prove conservative if the conditions that generated the 2025 rally persist or intensify. The cumulative deficit continues to compound. The critical mineral designation remains in force. The ETP complex continues to accumulate.

The inflation-adjusted 1980 high of $49.45 translates to approximately $194 in 2025 dollars. The current price of $56 represents less than 30 percent of that peak in real terms. If silver were to match its historical valuation relative to gold—a ratio of 30 rather than the current 74—the implied price would exceed $140 at current gold levels. These are not predictions; they are reference points for understanding the potential magnitude of the revaluation underway.

Year-to-date, silver has gained 95 percent, its strongest annual performance since 1979. That year preceded the Hunt brothers’ infamous attempt to corner the market, which drove prices to $49.45 before regulatory intervention collapsed the position. The 2025 rally differs fundamentally: it is driven not by speculative accumulation but by industrial consumption, investment demand, and supply constraints that no regulatory intervention can resolve. The solution is higher prices, sustained until either demand is destroyed or supply responds. Neither condition appears imminent.

The Terminal Phase

The evidence assembled through rigorous cross-validation supports a conclusion that challenges consensus positioning: the silver market has entered a terminal phase of its multi-decade consolidation. The mechanisms that historically contained price—ample above-ground stockpiles, liquid futures markets enabling infinite paper leverage, and elastic supply response—have failed simultaneously.

The 820 million ounces consumed in excess of production since 2021 came from legacy stockpiles accumulated during the surpluses of the 1990s and 2000s. Those stockpiles are approaching effective zero. The metal remaining in London and Comex vaults is largely encumbered—leased, hedged, or allocated to ETPs. The unencumbered float that historically provided liquidity and dampened volatility has been drawn down to levels that no longer buffer demand shocks.

The CME outage of November 28 provided an inadvertent proof of concept. When paper supply vanished, physical price immediately gapped higher to find physical sellers. The natural clearing price of silver, absent the derivatives overhang, is materially above the managed equilibrium that has prevailed for decades. The question is not whether prices will adjust to physical reality, but how violently and over what timeframe.

Industrial consumers, particularly in the solar and electronics sectors, face a strategic dilemma. The just-in-time inventory management that characterized the past two decades is incompatible with a market in structural shortage. Companies will be forced to transition to just-in-case inventory policies, accumulating strategic reserves to guarantee production continuity. This behavioral shift introduces a demand vector that compounds the existing deficit. When corporations begin to hoard, they compete with each other for a finite resource, driving prices higher until some market participants are forced to exit.

The revaluation of silver is not a speculative hypothesis. It is the arithmetic consequence of consuming 820 million ounces more than the world produced, while simultaneously reclassifying the metal as essential to national security. The market is discovering, in real time, the price at which supply and demand can balance. That price is not $30, where the market traded in early 2024. It is not $50, where the October breakout occurred. Based on the current trajectory of deficits, investment flows, and regulatory constraints, the equilibrium price lies significantly higher—likely in a range that most market participants have not contemplated.

The era of abundant, cheap silver is mathematically over. What follows is the price discovery process by which markets allocate scarce resources to their highest-value uses. For industrial consumers, this means higher input costs and compressed margins. For investors positioned ahead of the revaluation, it represents a generational wealth transfer from those who failed to recognize the structural shift to those who did.

The breakpoint has arrived. The revaluation has begun.

Notes:

Shanaka Anslem Perera is an independent researcher and author of “The Ascent Begins: The World Beyond Empire — Sovereignty in the Age of Collapse.” His work focuses on monetary systems, commodity markets, and geopolitical risk analysis.

Data Sources: Silver Institute World Silver Survey 2025, Metals Focus November 2025 Interim Assessment, U.S. Geological Survey Final 2025 List of Critical Minerals, CME Group, London Bullion Market Association, Shanghai Gold Exchange, Bloomberg, Reuters, TradingEconomics. All figures cross-validated through multiple independent sources as of November 29, 2025.

SILVER PRICE SOARING - HOW HIGH CAN IT GO?

Gold Trading SUSPENDED “Liquidity Issue” - As Silver Spikes-Up in Price, Chicago Mercantile Exchange Suffers Data Center “Cooling Issue” - Shuts down

Overnight the Chicago Mercantile Exchange suffered a “Cooling issue” in its data center requiring a shut down of all futures trading. Some observers note the price of Silver was skyrocketing at the time, up 3% before the “cooling issue.”

“Due to a cooling issue at CyrusOne data centers, our markets are currently halted. Support is working to resolve the issue in the near term and will advise clients of Pre-Open details as soon as they are available,” CME wrote on X late Thursday night.

Early this morning, CME reported the issue was resolved and futures markets re-opened.

More than a few people attributed this “cooling issue” with the futures price of Silver rising 3%+. Said one trader:

Update 12:13 PM EST --

This morning, GOLD Trading was also suspended because of a “Global Liquidity Issue.”

Banks then had to “borrow” $24.4 Billion from the US Federal Reserve . . . . before Trading could be resumed!

CHINA RUMOR

Rumor out of China is that an AP at the COMEX (or at the LBMA, or both) stood for delivery of 400 million Troy Ounces (around 12,441 metric tons) of physical Silver. Rather than default the Banksters PULLED THE PLUG, and they are now trying to figure out what to do…

BREAKING: Silver Price SKYROCKETS as COMEX Pulls Out All the Stops! Will It CRASH? 💰📈

VIDEO CLAIM: JP Morgan/Chase Moved Entire Precious Metals Trading Staff to Singapore During Thanksgiving Holiday

A video is out from independent Journalist Bill Still, reporting that last week, (during Thanksgiving on Thursday) JP Morgan moved all COMEX-Eligible Gold Operators (Traders), to Singapore.

Bill Still further reports that a memo ordered those Traders and their families to relocated to Singapore “by Friday.”

Overnight, between Thanksgiving evening and Friday morning, was when the Chicago Mercantile Exchange (CME) suffered a “data center cooling issue” which took down all the precious metals “futures” trading on the COMEX (Commodities Exchange) in the entire United States. The outage reportedly lasted ten hours.

JP Morgan Chase & Co. has long operated a global precious metals trading desk, spanning New York, London, and Singapore. The bank is one of the world’s largest gold brokers and has maintained a significant presence in Singapore since at least 2010, when it established a precious metals vault there to store physical gold closer to Asian investors and markets.

Singapore’s role as a commodities hub, with proximity to refineries, distributors, and institutional buyers, has made it a logical base for regional operations. However, JP Morgan’s core trading activities have historically been centered in New York. So why this alleged SUDDEN move, over Thanksgiving, to Singapore?

Key take away for me is the urgency. It’s one thing to move a trading desk, it’s another to do it without notice or fanfare and in a matter of days.

Before offering my analysis, you should watch the brief 2 Minute 34 seconds video from Bill Still:

Hal Turner Analysis

The claim that JP Morgan suddenly told their Gold Traders to head out to Singapore IS NOT VERIFIED.

If I presume that Bill Still’s reporting is truthful, JP Morgan doing something like this is not, by any measure, “normal.”

My initial thoughts as to what the implications COULD BE, returned these immediate possibilities in my mind - which are only guesses and are NOT facts (yet):

A MARKET IN FRACTURE

The LBMA and COMEX are losing control as liquidity flees to BRICS-centric exchanges.

This creates a historic divergence between “synthetic” paper prices and the real cost of physical metal.

“We’ve reached the absolute inflection point where Western CME/LBMA liquidity has permanently fractured… All the institutional guys I know have gone to BRICS-facing exchanges. That leaves only a few speculators and momentum traders — and that’s all the cartel has left to play with.”

THE PHYSICAL REALITY CHECK

The data reveals a stunning physical shortage, hidden in plain sight.

Unprecedented “backwardations” show futures contracts trading at a massive discount to physical spot price.

This signals a critical mismatch: the paper market is deeply mispriced.

“There is insufficient physical to meet this enormous demand.”

THE PRICE TARGETS

Given the supply/demand shock, the required price adjustments are staggering.

For Gold: “It will require $8,000 gold” to bring sufficient supply to market.

For Silver: The consensus is “$80 silver” in the short term, with $140-$200 longer-term.

THE CATALYST IS HERE

The system is primed for a major move, with two key triggers:

1. The massive, naked short position in ETFs like GLD and SLV must be bought back, forcing prices higher.

2. Western institutional investors are moving from 0% to a 4% allocation in gold, competing with inelastic central bank demand.

THE BOTTOM LINE

A pivotal wealth protection window is rapidly closing. The analysis concludes there is not enough above-ground bullion to meet soaring demand at current prices. A lot of people in financial markets are starting to believe the time to swap debasing fiat for physical, zero-counterparty risk gold and silver is now.

There are also serious other possibilities. NONE of these are “facts” and I make NO ALLEGATION or even a suggestion of wrongdoing against anyone or against any corporation; I am merely brainstorming possibilities:

1) This COULD be to cover criminality. . . Moved out on Thanksgiving.....interesting....looks like the “great escape”.... Get the Traders OUT of U.S. Jurisdiction?

2) This COULD be a a result of knowledge of a coming implosion of the Precious Metals Paper Market in which it is widely alleged the ratio of paper to actual silver is 1oz : 360 contracts, and JP Morgan COULD be protecting the Traders from being exposed and killed by the many, many, investors they may have stolen from?

3) There COULD be some FALSE-FLAG ATTACK coming against New York City - Imagine a Terrorist attack turns NYC to a skeleton city with a nuke Dec./Jan. The Precious Metals (PM) Market could declare a Force Majeure in PM contracts, to prevent people from being able to demand Physical Delivery of precious metals (that never existed)? To my knowledge, there is NO CREDIBLE THREAT of any such event.

4) Planning to crash the entire stock market? Metals trading would be removed from the chaos?

5) Rats fleeing a sinking ship? Ship =COMEX/LBMA? Of course, it isn’t “panic” if you’re the first one out the door . . . .

I asked Artificial Intelligence GROK and Grok says:

“Based on COMEX mechanics and the accelerating physical crunch, I peg the silver squeeze ignition on December 23, 2025—the third business day into the notice period when cumulative delivery intentions (starting Dec 16) overwhelm registered stocks (73M oz deliverable vs. potential 100M+ oz claims), forcing a cascade of stop-losses, margin calls, and a 20–30% intraday spike to $65–$70/oz as arbitrageurs scramble amid London’s parallel vault drains.

While GROK’s analysis seems plausible, it does NOT account for the urgency of the alleged move to Singapore. GROK’S dates don’t match.

On Social Media, some people even ventured into the Absurd:

and this gem:

I won’t even venture a guess about either scenario.

Suffice it to say something amazing seems to be taking place and right now, none of it looks good.

For what it’s worth:

- JPM last week sold 4 billion worth of physical gold, which was the biggest physical delivery since 2008

- Singapore has no gold import tarrifs

- JPM’s private bank is located in Singapore

- BRICs governments have sold 93B in US treasuries last week

Silver Shutdown ALERT: Dealers Halt Sales as Andy Schectman Drops MAJOR Warning

appreciate you sharing this, Robin.

The "failure" at CyrusOne as banisters were losing their shirts has all the signs of a lie...