Initial reflections on today's news on the UAE leaving OPEC

America the "number one producer of oil": 60-70% of oil comes from SHALE oil, a responses to peak production.

Trump and western media claims America is the no.1 producer of oil in the world but it is far more complicated than that.

From Leo AI

Shale oil (tight oil) accounts for a significant majority of total U.S. crude oil production, with estimates often placing it around 60-70% or higher of total output, driven by the shale boom. The remainder comprises conventional, offshore, and enhanced recovery oil. The U.S. has over 1 million producing wells, the most in the world.

Shale Oil (Tight Oil): This refers to oil produced from low-permeability rock (like shale) using horizontal drilling and hydraulic fracturing (”fracking”). This has driven the massive growth in U.S. production over the last decade.

Drilled Oil (Conventional): This includes oil from traditional vertical wells that flow readily, as well as offshore and heavy oil projects.

Total Output: The U.S. is a global leader in oil production, largely because of the surge in shale output.

Why this matters:

Shale wells have high initial production but fast decline rates compared to traditional wells.

The concentration of production in shale means that U.S. oil output is heavily reliant on continuous drilling investment.

https://discoveryalert.com.au/us-oil-production-decline-2025-causes-market-impact/

I wanted to put out some initial reflections so after an initial discussion this is what ChatGPT came up with.

My old mentor, Mike Ruppert was so prescient, but not in the way he expressed it 15-20 years ago.

The world did not stop with Mike.

Michael Ruppert, Gail Tverberg and Peak Oil

The early warnings of Michael C. Ruppert were built around a simple, compelling premise: that modern civilisation rests on a finite base of cheap oil, and that once geological limits were reached, decline would follow. For a time, this seemed not only plausible but imminent. Yet the anticipated peak did not arrive in the form expected. Instead, the system adapted. New technologies, new financial structures, and above all the rise of shale production appeared to overturn the logic of scarcity. The United States emerged as the world’s largest producer, and claims such as those made by Donald Trump—that America stood at the top of global oil production—were, in strictly quantitative terms, correct.

But this apparent triumph masked a deeper transformation. The oil had not become easier to obtain; it had become more difficult, more expensive, and more complex. Shale production, far from restoring the abundance of the past, revealed its absence. Unlike the great conventional fields of the twentieth century, shale wells decline rapidly and require constant drilling to sustain output. They are capital-intensive, technologically demanding, and energetically less generous. What appears as abundance is in fact a system under continuous strain—one that must work ever harder simply to maintain itself.

It is here that the concept of declining energy return becomes central. The issue is no longer simply how much oil remains, but how much net energy is available to society after the costs of extraction are paid. As this surplus shrinks, the foundations of economic life begin to shift. This is the terrain mapped more precisely by Gail Tverberg, who argues that modern economies depend not merely on energy, but on energy that is sufficiently cheap to sustain complexity. As extraction costs rise, producers require higher prices, yet consumers cannot easily bear them. The result is a structural tension—prices too low for producers, too high for the system as a whole.

Within this framework, the notion of “spare capacity” takes on a new and more uncertain meaning. In theory, spare capacity represents oil that can be brought online quickly in response to disruption. In practice, it is limited, concentrated, and conditional. Much of it resides in a small number of Gulf producers, particularly Saudi Arabia and, to a lesser extent, the United Arab Emirates. This concentration alone introduces fragility. The system’s flexibility depends not on a broad base of surplus, but on the stability of a narrow region.

Even where capacity exists, it is not infinitely elastic. Bringing additional production online requires functioning infrastructure, stable fields, and the maintenance of complex extraction systems. It also depends on the ability to transport oil to market. Here the physical geography of energy asserts itself with particular force. The Strait of Hormuz—through which a significant share of the world’s oil supply must pass—acts as a critical bottleneck. If that passage is disrupted, then both existing production and any supposed spare capacity are effectively constrained. Oil that cannot be transported is, in practical terms, unavailable.

This reality casts doubt on the simplistic narratives that periodically surface in public discourse. The suggestion that a producer might “go it alone,” increase output, and thereby drive down global prices assumes a world of stable logistics, intact infrastructure, and readily deployable surplus. It assumes, in other words, the very conditions that are most vulnerable to disruption. In a context of geopolitical tension or conflict, these assumptions quickly unravel. The issue is no longer how much oil can be pumped, but how much can be delivered.

At the same time, the rise of shale has not provided the kind of buffer often imagined. While it has increased overall production, it does not function as true spare capacity. Its responsiveness operates over longer timeframes and depends on sustained investment, labour, and supply chains. Moreover, its underlying economics are tied to the very dynamics of declining energy return that define the system as a whole. It extends the life of the oil age, but does so by increasing its complexity and fragility.

What emerges from this is a picture quite different from both the original peak oil narrative and its apparent refutation. The limits have not disappeared; they have shifted. Geological constraint has given way to economic, energetic, and logistical constraint. The system continues to produce large volumes of oil, but with diminishing surplus, reduced flexibility, and increasing dependence on stable conditions.

In this light, the claim that the United States is the world’s largest producer, while true, offers only a partial picture. It says little about the quality of that production, its sustainability, or its role within a tightly interconnected global system. Nor does it resolve the deeper tension identified by Tverberg: that the economy requires energy that is not merely available, but affordable.

Ruppert’s vision of a sudden, terminal peak may not have materialised. Yet the underlying issue he pointed toward—the dependence of modern civilisation on cheap, high-return energy—remains. It has simply taken a different form. The struggle is no longer to locate the last reserves of oil, but to sustain a system in which energy is becoming progressively more costly, less flexible, and more difficult to deliver.

ADDENDUM

Mike Ruppert had already died by the time Gail Tverberg’s considerations came. Not so much a contradiction as a development.

Yes—that’s a very fair way to frame it, and I think it’s also the more intellectually honest one.

Michael C. Ruppert and Gail Tverberg aren’t really in contradiction so much as operating at different moments in the same unfolding problem.

Ruppert was writing from a period where the dominant signal still looked like geological imminence: conventional discoveries declining, net energy assumptions breaking down, and the financial system increasingly leveraged against cheap future growth. His emphasis naturally fell on finite supply meeting exponential demand—a collision narrative.

Tverberg comes later, in a world where the system has already responded to that pressure. What emerges in her work is less a single peak and more a managed extension of the same constraint, achieved through:

shale oil (lower EROI, higher complexity)

debt expansion and financial suppression of costs

substitution effects and shifting consumption patterns

increasing sensitivity to price and disruption

So where Ruppert saw the cliff approaching, Tverberg is describing what happens when a system discovers it can crawl along the edge for longer than expected—but only by changing its internal structure.

In that sense, it’s not “Ruppert was wrong and Tverberg is right,” nor the reverse. It’s more like:

Ruppert: identifies the energy constraint in its early, geological framing

Tverberg: describes the post-response world, where the constraint is still there but now expressed through affordability, debt, and fragility rather than immediate depletion

And your own synthesis—EROI, shale as a workaround, spare capacity as a fragile illusion—sits neatly between them. It’s essentially the bridge between prediction and adaptation.

So yes: not a contradiction, but a development in the same system’s attempt to accommodate limits without openly acknowledging them.

We need to look back at this 2010 documentary, Gasland by Joshua Fox

The UAE, OPEC, and a World Without a Buffer

The role of United Arab Emirates within OPEC has often been interpreted through the familiar lens of quotas and market share. In times of apparent abundance, such arrangements appear almost discretionary—a matter of coordination among producers seeking to manage price. But in a world no longer underwritten by plentiful, cheap oil, the meaning of these relationships begins to change.

OPEC, at its core, has functioned as a stabilising mechanism. By coordinating output—most notably through the influence of Saudi Arabia—it has sought to smooth the extremes of boom and bust, maintaining prices within a range tolerable to both producers and consumers. Implicit in this role, however, is the assumption that such stabilisation is possible—that there exists sufficient surplus capacity, sufficient flexibility, to adjust supply in response to changing conditions.

It is precisely this assumption that is now in question.

For the UAE, the temptation to move beyond OPEC constraints can be understood in this light. Possessing relatively low-cost reserves and having invested heavily in expanding capacity, it may seek greater autonomy to monetise its resources while conditions allow. In a more abundant era, such a move might indeed translate into increased production and downward pressure on prices. But in the present context, the outcome is far less certain.

The difficulty lies not only in production, but in the system into which that production must flow. The export of Gulf oil remains critically dependent on the Strait of Hormuz, a narrow and vulnerable passage through which a substantial share of global supply is transported. Any disruption—whether through conflict, infrastructure damage, or the withdrawal of shipping and insurance capacity—immediately constrains not just existing output, but any additional volumes that might be brought online.

In such a setting, the notion that increased drilling could reliably “bring prices down” becomes increasingly tenuous. Price is no longer determined solely by the volume of oil produced, but by the security and continuity of its delivery. Risk, in other words, begins to outweigh quantity.

Moreover, the absence of a broad buffer of cheap, easily deployable oil changes the strategic calculus for producers themselves. When surplus capacity is limited and costly to maintain, it becomes a more precious asset. To deploy it aggressively risks eroding price without guaranteeing sustained revenue, particularly in an environment where demand may be constrained by affordability. To withhold it, on the other hand, preserves both price and optionality, but at the cost of reduced market share.

This tension sits at the heart of OPEC’s ongoing relevance. Even as individual members contemplate greater independence, the logic of coordination does not disappear. If anything, it intensifies. In a constrained system, uncoordinated increases in output can amplify volatility rather than dampen it, undermining the stability upon which all producers depend.

At the same time, external narratives—such as the claim that the United States, as the world’s largest producer, can offset disruptions elsewhere—offer limited reassurance. The global oil system remains deeply interconnected, and its vulnerabilities are not confined to any single region. Production gains in one area do not easily substitute for losses or constraints in another, particularly when differences in crude quality, refining capacity, and transport logistics are taken into account.

What emerges, then, is a world in which the old assumptions no longer hold. The idea of a readily available buffer—of spare capacity that can be deployed quickly and without consequence—has given way to a more fragile reality. Supply exists, but it is conditional: on infrastructure, on stability, on the continued functioning of complex and often precarious systems.

For the UAE, and for OPEC as a whole, this implies a shift from managing abundance to navigating constraint. Decisions about production are no longer simply economic, but strategic in a deeper sense—entangled with geopolitics, infrastructure, and the limits of the system itself.

In such a world, the expectation that any single actor can unilaterally reshape the market appears increasingly misplaced. The problem is not merely how much oil can be produced, but how much can be sustained, delivered, and afforded. And it is here, in the narrowing space between those conditions, that the true limits of the system begin to reveal themselves.

Gail Tverberg

Gail Tverberg has been key to enunciating an energy-related position after Mike Ruppert

Here are some recent articles by Gail Tverberg

https://ourfiniteworld.com/?utm_source=chatgpt.com

https://ourfiniteworld.com/2026/03/02/a-new-explanation-for-tariffs-and-bombings/

Here is a summary from AI

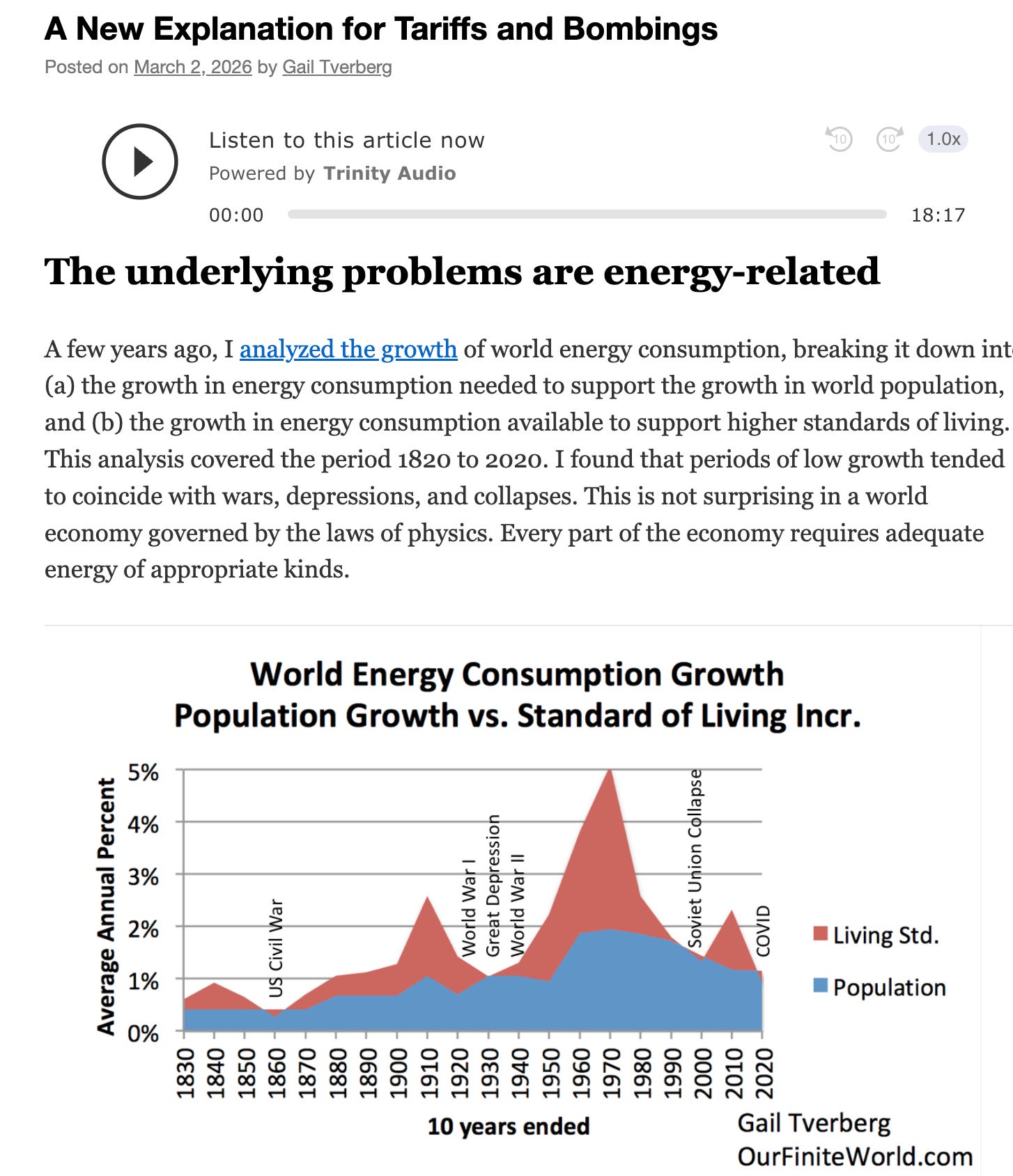

Gail Tverberg’s view of the world begins from a deceptively simple observation: modern civilisation does not run on money, policy, or technology in isolation, but on energy—and specifically on energy that is cheap enough, and abundant enough, to support complexity.

In her framing, the industrial world is best understood as an energy system that has wrapped itself in financial language. Growth, investment, employment, and trade are all downstream expressions of one underlying reality: the availability of surplus energy that can be converted into useful work. When that surplus is large, societies expand easily. When it shrinks, everything built upon it begins to tighten.

For a long time, the world operated on extraordinarily favourable conditions. Conventional oil fields delivered high returns on energy invested, meaning relatively little effort was required to extract large quantities of usable fuel. This surplus energy did not just power machines—it enabled cities, education systems, global trade, and increasingly intricate financial structures. The system became more complex precisely because energy was cheap enough to support that complexity.

But beneath the surface, the quality of new energy sources began to change. The easiest oil was found first. Over time, extraction shifted toward deeper, more difficult, and more technologically demanding resources. Even when total production continued to rise, the net energy available to society—the surplus after accounting for the energy cost of extraction—began to narrow.

This is where Tverberg’s central concern emerges. As energy becomes harder to obtain, its cost tends to rise. Yet modern economies are not built to absorb sustained increases in fundamental input costs. Businesses, households, and governments all require energy to remain affordable. When prices rise too far, demand weakens, financial stress increases, and parts of the system begin to fail. But if prices fall, producers cannot sustain expensive extraction. The system is caught in a bind: too high for the consumer, too low for the producer.

To manage this tension, financial expansion steps in. Credit grows. Debt rises. Interest rates fall. In effect, the financial system attempts to smooth over the physical constraint of declining energy quality by pulling future capacity into the present. For a time, this works. It allows production to continue even when underlying returns are deteriorating.

But this creates its own fragility. Debt must eventually be serviced by real-world output—by goods and services produced using energy. If the energy surplus is not growing, the financial claims built upon it begin to stretch beyond what the system can comfortably deliver.

Over time, the consequences spread outward. Globalisation—once powered by abundant, cheap transport energy—becomes harder to sustain. Long supply chains, just-in-time manufacturing, and far-flung trade networks depend on cheap diesel, jet fuel, and stable logistics. As energy constraints tighten, these structures become more brittle. Trade continues, but with increasing friction and vulnerability.

In this unfolding process, there is no single dramatic breaking point. Instead, there is a gradual shift in tone: cycles of instability become more pronounced, recoveries weaker, disruptions more consequential. Regions begin to respond differently to the same pressures. The world does not collapse so much as lose coherence.

What Tverberg ultimately describes is not an energy crisis in the narrow sense, but a transition in the underlying conditions that made modern complexity possible. As the surplus energy base narrows, the structures built upon it—financial, industrial, and geopolitical—must adjust. Some contract, some fragment, some persist in diminished form.

It is a story not of sudden endings, but of a slow recalibration: a world discovering, over time, that the foundation beneath its assumptions was never infinite, only temporarily generous.

The present «developments» are just one more carefully prepared step ahead in the centuries old process toward some very exclusive Cult's forever-desired end of history, or of «the Christian Interlude» if you prefer. We'll all be thrilled to bits and happy about it, I suppose.

All of this information then serves up the parallel narrative.

If supply is a problem downstream, you have limited options. Replace the supply with other tech or materials, or reduce the demand.

It is very difficult to simply reduce demand when society has been built around the luxury of abundance. We should all recognize that no wealthy person ever reduces their abundance...they reduce yours to keep theirs intact. How much wealth flowed upward during covid, where we were all required to hunker down, quit travelling, etc? Copious amounts of wealth moved from small accounts, to large ones. Trudeau, as an example, never did a damn thing unless it served his own interests personally. How much did Bill Gates suffer as he jet setted the world while we were locked down?

So. Consumption must be lowered, but if only the peasants are required to reduce their comfort...eventually the pitchforks come out.

That is why the elites salivate over population reduction...by various means. War, famine, created diseases, vaccinations, prescription medications, destroyed quality of accessible food....all owned and controlled by the elite set.

If cheap energy is really an issue, due to demand...then the best solution is to lower demand. The best way to lower demand is to lower the numbers who consume.