June 9, 1974: MILESTONE’ PACT IS SIGNED BY U.S. AND SAUDI ARABIA

June 9, 1974: MILESTONE’ PACT IS SIGNED BY U.S. AND SAUDI ARABIA

Hal Turner, on his radio show said he could nt find the pact. It took me about a minute to find this

MILESTONE’ PACT IS SIGNED BY U.S. AND SAUDI ARABIA

By Bernard Gwertzman Special to The New York Times

June 9, 1974

This is a digitized version of an article from The Times’s print archive, before the start of online publication in 1996. To preserve these articles as they originally appeared, The Times does not alter, edit or update them.

Occasionally the digitization process introduces transcription errors or other problems; we are continuing to work to improve these archived versions.

WASHINGTON, June 8—The United States and Saudi Arabia today signed a wide‐ranging military and economic agreement that both said “heralded an era of increasingly close cooperation.”

American officials, commenting on the first such arrangement between the United States and an Arab country, said that they hoped the new accord would provide Saudi Arabia with incentives to increase her oil production and would serve as a model for economic cooperation between Washington and other Arab nations.

Secretary of State Kissinger and Prince Fand Ibn Abdel Aziz, Second Deputy Premier of Saudi Arabia and a half‐brother of King Faisal, signed the six‐page agreement at Blair House across the street from the White House this morning.

Acclaimed by Kissinger

Mr. Kissinger, who will accompany President Nixon on a tour of the Middle East next week, including a stop in Saudi Arabia, said, “We consider this a milestone in our relations with Saudi Arabia and with the Arab countries in general.”

Prince Fand said that the accord was “an excellent opening in a new and glorious chapter in relations between Saudi Arabia and the United States.”

The agreement establishes two joint commissions, one on economic cooperation and the other on Saudi Arabia's military needs.

The economic commission will hold its first meeting in October in Saudi Arabia. It will be composed of members drawn from the State Department, the Treasury, the Commerce Department, the National Science Foundation and other American agencies as well as comparable Saudi Government bodies.

Working Groups Set Up

In the meantime, four joint working groups were created to prepare recommendations and plans for the economic commission. They were the following:

¶A group on industrialization that will meet in Saudi Arabia en July 15 “to consider plans for Saudi Arabia's economic development, paying special attion to the use of flared gas for expanding the production of fertilizer.” Flared gas is the gas burned off at the well, head in the production of oil. In properly harnessed, it provides a potential raw material for the manufacture of fertilizer.

¶A group on manpower and education “to consider projects aimed at the further development of Saudi technical manpower skills, the expansion of educational and technical institutions, the transfer of technological expertise, the establishment of a comprehensive Saudi Arabian science and technology program keyed to the national goals of the kingdom, and an expansion of sister university relations.” The group will meet “shortly” in Saudi Arabia.

¶A group on technology, research and development that will examine specific cooperative projects in such fields as solar energy and desalination.

¶A group to examine agricultural development proposals, in particular desert agriculture.

The two Governments also agreed to consider setting up an economic council to foster cooperation in the private sector. The Treasury Department and the Saudi Arabian Ministry of Finance and National Economy “will consider cooperation in the field of finance,” the agreement said.

For more than 20 years, the United States has provided technical help and sold military equipment to Saudi Arabia's armed forces. The newly created military commission, the accord said, “will review programs already under way for modernizing Saudi Arabia's armed forces in light of the kingdom's defense requirements especially as they relate to training.”

The security situation in the Arabian Peninsula was reviewed in the talks that Prince Fand held with Mr. Nixon, Mr. Kissinger and other American officials in his three days here. “It was recognized,” the agreement said, “that responsibility for maintaining security and promoting orderly development in this area belonged to the states of the region and that close cooperation among them is needed for thir security.”

“The United States,” it went on, “expressed its continuing support for cooperative measures.”

American officials reported that the entire range of Middle East diplomatic questions was also discussed and the agreement said that both sides “expressed satisfaction” with the progress made so far toward an Arab‐Israeli solution.

Although Saudi Arabia has the world's largest proven reserves of oil, the agreement did not mention the word oil. Both sides wanted to avoid the impression that these were bilateral talks on oil.

More Output Sought

American officials, however, have made no secret of their hope that Saudi Arabia will take the lead in increasing production of oil—now at about 8.6 million barrels a day—and that way help bring about drop in the world price.

If Saudi Arabia's industrial capacity, is increased, the thinking here goes, she will want to spend more money earned from oil on technology and equipment in the United States, and this should lead to a rise in output. The sale of sophisticated military equipment, such as modern jet fighters, would also absorb some of the oil money.

Mr. Nixon can be expected to discuss joint commissions with other Arab leaders one his trip, which will take him to Egypt, Jordan, Syria and Saudi. Arabia as well as Israel.

Nixon at Camp David

Mr. Nixon spent the day at Camp David preparing for his departure on Monday morning and refund to the White House this evening. He is expected to address a lunch tomorrow of the Commitee for Fairness to the Presidency, a group opposed to his impeachment.

The first stop will be Salzburg, Austria, where Mr. Nixon will meet with Chancellor Bruno Kreisky on Tuesday. On the same day, Mr. Kissinger will meet with the West German Foreign Minister, HadsDietrich Genscher, at an undisclosed location near the Austrian border.

From Bloomberg, 2016

The untold story behind Saudi Arabia’s 41-year US debt secret

NEW YORK: Failure was not an option. It was July 1974. A steady predawn drizzle had given way to overcast skies when William Simon, newly appointed US Treasury secretary, and his deputy, Gerry Parsky, stepped onto an 8 am flight from Andrews Air Force Base. On board, the mood was tense. That year, the oil crisis had hit home. An embargo by OPEC’s Arab nations — payback for US military aid to the Israelis during the Yom Kippur War — quadrupled oil prices.

Inflation soared, the stock market crashed, and the US Economy was in a tailspin. Officially, Simon’s two-week trip was billed as a tour of economic diplomacy across Europe and the Middle East, full of the customary meet-and-greets and evening banquets. But the real mission, kept in strict confidence within President Richard Nixon’s inner circle, would take place during a four-day layover in the coastal city of Jeddah, Saudi Arabia.

The goal: neutralise crude oil as an economic weapon and find a way to persuade a hostile kingdom to finance America’s widening deficit with its newfound petrodollar wealth. And, according to Parsky, 73 — one of the few officials with Simon during the Saudi talks — Nixon made clear there was simply no coming back empty-handed. Failure would not only jeopardise America’s financial health but could also give the Soviet Union an opening to make further inroads into the Arab world.

Simon, who before being tapped by Nixon ran the vaunted Treasuries desk at Salomon Brothers, understood the appeal of US government debt and how to sell the Saudis on the idea that America was the safest place to park their petrodollars. With that knowledge, the administration hatched an unprecedented do-or-die plan that would come to influence just about every aspect of US-Saudi relations over the next four decades (Simon died in 2000 at the age of 72). The basic framework was strikingly simple. The US would buy oil from Saudi Arabia and provide the kingdom military aid and equipment. In return, the Saudis would plough billions of their petrodollar revenue back into Treasuries and finance America’s spending.

It took several discreet follow-up meetings to iron out all the details, Parsky said. But at the end of months of negotiations, there remained one small, yet crucial, catch: King Faisal bin Abdulaziz Al Saud demanded the country’s Treasury purchases stay “strictly secret,” according to a diplomatic cable obtained by Bloomberg from the National Archives database.

The secret was kept for more than four decades — until now. In response to a Freedom-of-Information-Act request submitted by Bloomberg News, the Treasury broke out Saudi Arabia’s holdings for the first time this month after “concluding that it was consistent with transparency and the law to disclose the data,” according to spokeswoman Whitney Smith. The $117 billion trove makes the kingdom one of America’s largest foreign creditors. Yet in many ways, the information has raised more questions than it has answered. A former Treasury official specialising in central bank reserves, who did not want to be identified, says the official figure vastly understates Saudi Arabia’s investments in US government debt, which may be double or more. The current tally represents just 20% of its $587 billion of foreign reserves, well below the two-thirds that central banks typically keep in dollar assets.

Exactly how much of America’s debt Saudi Arabia actually owns is something that matters more now than ever before. While oil’s collapse has deepened concern that Saudi Arabia will need to liquidate its Treasuries to raise cash, a more troubling worry has also emerged: the spectre of the kingdom using its outsize position in the world’s most important debt market as a political weapon, much as it did with oil in the 1970s.

In April, Saudi Arabia warned it would start selling as much as $750 billion in Treasuries and other assets if Congress passes a bill allowing the kingdom to be held liable in US courts for the September 11 terrorist attacks, according to the New York Times. The threat comes amid a renewed push by presidential candidates and legislators from both the Democratic and Republican parties to declassify a 28-page section of a 2004 US government report that is believed to detail possible Saudi connections to the attacks. The bill, which passed the Senate on May 17, is now in the House of Representatives. Saudi Arabia’s Finance Ministry declined to comment on the potential selling of Treasuries in response. The Saudi Arabian Monetary Agency didn’t immediately answer requests for details on the total size of its US government debt holdings.

Saudi Arabia, which has long provided free health care, gasoline subsidies, and routine pay raises to its citizens with its petroleum wealth, already faces a brutal fiscal crisis. Saudi Arabia’s situation has become so acute the kingdom is now selling a piece of its crown jewel —state oil company Saudi Aramco. What’s more, the commitment to the decades-old policy of “interdependence” between the US and Saudi Arabia, which arose from Simon’s debt deal and ultimately bound together two nations that share few common values, is showing signs of fraying. “Buying bonds and all that was a strategy to recycle petrodollars back into the US,” said David Ottaway, a Middle East fellow at the Woodrow Wilson International Center in Washington. But politically, “it’s always been an ambiguous, constrained relationship.”

Yet, back in 1974, forging that relationship (and the secrecy that it required) was a no-brainer, according to Parsky, who is now chairman of Aurora Capital Group, a private equity firm in Los Angeles. Many of America’s allies, including the UK and Japan, were also deeply dependent on Saudi oil and quietly vying to get the kingdom to reinvest money back into their own economies. “Everyone — in the US, France, Britain, Japan — was trying to get their fingers in the Saudis’ pockets,” said Gordon S Brown, an economic officer with the State Department at the US embassy in Riyadh from 1976 to 1978.

For the Saudis, politics played a big role in their insistence that all Treasury investments remain anonymous. Tensions still flared 10 months after the Yom Kippur War, and throughout the Arab world, there was plenty of animosity toward the US for its support of Israel. According to diplomatic cables, King Faisal’s biggest fear was the perception Saudi oil money would, “directly or indirectly,” end up in the hands of its biggest enemy in the form of additional US assistance.

Treasury officials solved the dilemma by letting the Saudis in through the back door. In the first of many special arrangements, the US allowed Saudi Arabia to bypass the normal competitive bidding process for buying Treasuries by creating “add-ons.” Those sales, which were excluded from the official auction totals, hid all traces of Saudi Arabia’s presence in the US government debt market. By 1977, Saudi Arabia had accumulated about 20% of all Treasuries held abroad, according to The Hidden Hand of American Hegemony: Petrodollar Recycling and International Markets by Columbia University’s David Spiro.

Another exception was carved out for Saudi Arabia when the Treasury started releasing monthly countryby-country breakdowns of US debt ownership. Instead of disclosing Saudi Arabia’s holdings, the Treasury grouped them with 14 other nations, such as Kuwait, the United Arab Emirates and Nigeria, under the generic heading “oil exporters” — a practice that continued for 41 years.

From January, 2024. A very intelligent article

How & Why Petrodollar could end soon

Harshad Shah, Chartered Accountant at Independent Practice

Published Jan 14, 2024

What Are Petrodollars?

Petrodollars refer to the revenues generated from the export of crude oil, with the distinctive feature of being denominated in U.S. dollars. Coined in the mid-1970s, the term gained prominence during a period of surging oil prices that led to substantial trade and current account surpluses for nations heavily involved in oil exports. The prevalence of petrodollars stems from the enduring use of the U.S. dollar as the primary currency in international transactions. The widespread acceptance of the U.S. dollar in global trade is not solely reliant on the willingness of oil-exporting countries. Instead, it is rooted in the United States' status as the world's largest economy and principal importer of goods. Moreover, the U.S. dollar's preeminence is bolstered by the depth and liquidity of its capital markets, underpinned by the rule of law and military strength. Key facets of petrodollars include:

a) Payment in U.S. Dollars: Petrodollars represent U.S. dollars paid to nations engaged in oil exports.

b) Revenue Source for Oil Exporters: Many members of the Organization of the Petroleum Exporting Countries (OPEC) and other oil-exporting nations rely heavily on petrodollars as their primary source of revenue.

c) Denomination in Dollars: Oil-exporting countries settle their sales in U.S. dollars due to its widespread use, facilitating the investment of export proceeds.

d) Potential Alternatives: Some crude oil exporters, particularly those implicated in human rights violations, have hinted at the possibility of accepting payment in currencies other than the U.S. dollar.

In recent years, the global landscape of crude oil exports has witnessed significant changes. Before the onset of the COVID-19 pandemic, global crude oil exports averaged around 70 million barrels per day. By 2023, this figure had surged to 101.7 million barrels per day. The substantial market size, measured by revenue, of the Global Oil & Gas Exploration & Production industry reached $5.3 trillion in 2023. Considering an average price of $100 per barrel, this robust pace would translate into an annual global petrodollar supply exceeding $2.5 trillion. The dynamics of petrodollars remain integral to the intricate interplay of global energy markets and international finance.

Petrodollars, the Beginning and End

The Beginning: In 1971, Richard Nixon's decision to end the dollar's gold backing led to economic turmoil, known as stagflation. With the U.S. facing devalued currency, high unemployment, and soaring living costs, a solution was sought. In 1973, Secretary of State Henry Kissinger secured a deal with Saudi Arabia to exclusively sell oil globally in dollars, boosting demand for the weakening currency. This strategic move allowed the U.S. to sustain trade deficits, as countries exchanged dollars for oil. OPEC countries further fueled the U.S. economy by reinvesting their dollar profits into American bonds, enabling the U.S. to finance its government and run trade deficits without severe financial consequences.

Big Oil & Petrodollar: Big Oil, comprising major oil and gas companies like BP, Chevron, Eni, ExxonMobil, Shell, and TotalEnergies, wields significant economic power and political influence. As America became a net oil exporter, fueled by practices like hydraulic fracturing, environmental concerns emerged. However, the pivotal role of the U.S. dollar in global trade traces back to a 1970s agreement between the U.S. and Saudi Arabia, anchoring oil pricing in USD. This arrangement, coupled with the dominance of American oil benchmarks (West Texas Intermediate and Brent crude), solidified the USD's prominence. The world's growing reliance on oil, particularly in emerging economies like China, has reshaped global dynamics. China's rise, marked by strategic partnerships and initiatives like the Belt and Road, challenges U.S. economic dominance. Recent developments, such as a landmark 50-year agreement with Saudi Arabia, signal a shift away from the USD in oil trades. This shift underscores China's increasing influence and represents a significant step toward a global economy less dependent on the United States.

US’ economic dominance was built on the petrodollar

The economic dominance of the United States has historically been tied to the petrodollar system. The U.S. dollar's strength as a reserve currency is not only a reflection of the robust U.S. economy but also stems from the dollar's liquidity, partly due to countries maintaining dollar reserves for oil transactions. This link was established in the early 1970s after President Richard Nixon decoupled the dollar from gold. In 1974, a significant deal between Washington and Riyadh allowed Saudi Arabia to buy U.S. treasury bills before public auctions, in exchange for selling oil exclusively in dollars. This arrangement expanded the dollar's liquidity, and subsequent efforts led by Saudi Arabia influenced other OPEC nations to invoice oil in dollars.

The potential shift from the dollar to the Yuan in the global oil trade could have profound effects on both China and the U.S. If the Yuan displaces the dollar to a significant extent, countries might need to maintain Yuan reserves. This could lead to increased spending on Chinese debt and imports, strengthening China's economy while impacting the U.S. economy. The current disregard for the petrodollar by some nations, particularly highlighted by Saudi Arabia's evolving stance, has geopolitical implications. The emergence of bilateral arrangements and the avoidance of the dollar by major players like China, Russia, and India raise questions about the future of the petrodollar and the U.S. dollar as the world's reserve currency. The recent issuance of substantial Treasury Bonds by the U.S., coupled with shifts in buying patterns by major holders like China and Russia, suggests potential pressure on the U.S. dollar. Factors such as inflation and geopolitical events, including the Ukraine war, are contributing to a reevaluation of the global order. The evolving dynamics may be steering us towards a multipolar world, challenging the established norms and setting the stage for a reset in the global economic landscape. The unfolding events make for an interesting and challenging period ahead, with uncertainties about the future trajectory of the world order.

Petrodollar & the Lost American Century?

The world underwent a profound transformation on September 11, 2001, and later, on March 19, 2003, with the US-led invasion of Iraq. These events marked pivotal moments that could have shaped America's destiny positively but seem to have led to a squandering of potential and a shift towards fear, oppression, and economic decline. The 20th century, often termed "The American Century," boasted achievements in stabilizing global affairs and technological advancements. However, the 21st century appears marked by a departure from America's original purpose and promise. The American presence in the world, overshadowed by an authoritarian state, is characterized by pushing its model onto other societies and safeguarding corporate interests through manipulation and intimidation. This aspect of American foreign policy, involving overt and covert military and intelligence actions, remains largely unexplored in public discourse, obscured by government security measures.

During the Cold War era, force projections were often driven by geopolitical struggles with the Soviet Union. This led to interventions that protected some nations but trampled others. Allies' imperial ventures contributed to American involvement in regions where vital interests were not at stake. The arbitrary post-World War I drawing of Iraq's boundaries and manipulations of nations in the Middle East during the Cold War exemplify this.

The current situation reveals ongoing interference in other countries' affairs, such as the overthrow of Iran's democracy in 1953, support for Osama bin Laden, and current involvement in Venezuela. Covert and overt operations over decades have contributed to anti-American sentiments, creating blowback.

Operation Iraqi Freedom, characterized by "shock and awe," led to the destruction of a nation of 24 million people, marking an expensive and morally compromised chapter. The US's attempt to clean up the aftermath in Iraq seems destined for failure, signaling an entry into a Never-ending War and a forfeiture of the moral high ground. The American Century's legacy appears at risk of being overshadowed by the consequences of recent choices and actions.

Petrodollar Recycling: Petrodollar recycling is the practice of oil-exporting countries investing their U.S. dollar revenue, recognizing the dollar's global prominence for investments. This preference arises from the dollar's convenience as a store of value, essential for accumulating and earning returns on oil revenue. An early instance of petrodollar recycling occurred in 1974, with a U.S.-Saudi Arabia deal directing Saudi petrodollars into U.S. Treasuries. Subsequent agreements involved using Saudi oil export proceeds for U.S. aid, development projects, and financing arms sales to Saudi Arabia. Today, many oil-exporting nations invest their petrodollars in various financial instruments through sovereign wealth funds. Norway's sovereign wealth fund, for instance, holds around $1.4 trillion in assets as of 2021, with a significant allocation to stocks, making it a major player in the global equity market.

Role of Petrodollar in Dollar as Reserve Currency

The petrodollar system has significantly bolstered the U.S. dollar's status as the world's primary reserve currency. This system, where oil transactions are predominantly conducted in U.S. dollars, has had profound implications for global trade and finance. Key aspects include:

a) Oil Trade Denominated in U.S. Dollars: Most international oil transactions, particularly by OPEC members, are priced and sold in U.S. dollars, creating a consistent demand for the currency.

b) Dollar Recycling: Oil-exporting countries receive payment in U.S. dollars, often reinvesting excess dollars in U.S. financial assets. This process, known as "dollar recycling," contributes to the dollar's liquidity.

c) Alternatives to Petrodollar System: Despite proposals for alternatives, such as a basket of currencies or a new global currency, none have gained widespread support. Crypto currencies are a potential alternative, offering decentralization and reduced dependence on the U.S. dollar.

d) Dollar as the Preferred Reserve Currency: Central banks worldwide hold substantial reserves in U.S. dollars due to the stability of the U.S. economy, the liquidity of its financial markets, and the widespread acceptance of the dollar in international trade.

e) Global Trade and Finance: The dominance of the U.S. dollar in the oil trade extends to other areas of global trade and finance. Many international transactions, contracts, and commodities are priced and settled in U.S. dollars, reinforcing its role in the global economy.

f) Impact on Exchange Rates: The petrodollar system influences exchange rates, as countries relying on oil imports must acquire U.S. dollars. This constant demand supports the value of the dollar.

While the petrodollar system has played a crucial role, alternatives have been proposed. However, the likelihood of its immediate replacement is low. Exploring new options remains essential for ensuring the stability and security of the global economy.

Exploring De-Dollarization in a multi polar world

In a shifting global landscape, the dominance of reserve currencies has historically mirrored the economic fortunes of leading nations. Currently, the U.S. dollar holds this position, but signs of change are emerging. The slowing U.S. economy, coupled with trade wars and sanctions, especially after the Russia-Ukraine conflict, has spurred the de-dollarization movement. De-dollarization involves reducing reliance on the U.S. dollar for reserves, trade, and bilateral agreements. This trend is evident in several regions:

a) Russia: Hit by U.S.-led sanctions, Russia is shifting away from the dollar in bilateral trade, opting for non-dollar currencies. Pre-war, the use of USD in Russia's exports to BRICs nations significantly decreased.

b) China: Beijing is actively promoting the Yuan as an alternative to the dollar in international trade. China avoids USD-based transactions in bilateral trade, signing agreements with Iran, Canada, and Qatar to that effect.

c) India: India's central bank allows International Trade Settlement in Indian Rupees, facilitating trade and supporting the interests of the global trading community in INR. Bilateral trade settlements in INR have been established, with about 35 nations expressing interest.

d) Alternative for SWIFT: Russia and China are exploring a new payment system, combining the Russian SPFS with the Chinese CIPS, bypassing SWIFT.

e) BRICS Currency: Talks of a BRICS currency are increasing, reflecting a collaborative effort among emerging economies.

Reserve currencies historically last around 96 years on average, with the dollar's ascendancy dating back to 1920. The U.S. became a superpower in 1945, and the evolving dynamics suggest that the era of dollar dominance may be undergoing a transformative shift, ushering in a multi-polar world.

Are petrodollars fueling war & oppression?

The role of petrodollars in global affairs raises questions about their impact on war and oppression, particularly evident in instances like Saudi human rights violations and Russia's invasion of Ukraine. The vast wealth generated by oil exports can be wielded for either positive or negative purposes. The real problem with petrodollars lies in their potential misuse. While recycling petrodollars into investments or domestic development can yield positive outcomes, concerns arise when these funds are used to support domestic oppression, fuel an arms race, or engage in wars abroad. Recent incidents, such as the murder of Jamal Khashoggi by Saudi state agents and Russia's invasion of Ukraine, have intensified worries that petrodollars may be funding human rights violations and conflicts, often shielding those responsible from accountability.

a) Petrodollars as a Tool for Power: The connection between petrodollars and geopolitical power is explored in concepts like "Petrodollar Warfare." This term delves into hidden strategies employed by the power elite, shedding light on how big oil and political agendas intersect. The Iraq war is cited as an example, with the Euro currency's link to Iraq's oil pricing identified as a factor influencing the decision to topple Saddam Hussein.

b) Geostrategic Considerations: The manipulation of petrodollars reveals the intertwined nature of economic interests and political maneuvering. Understanding these dynamics is crucial for unraveling the complex motivations behind conflicts and interventions.

c) Impact on Human Rights: The oil wealth of certain nations, such as Saudi Arabia, has been associated with human rights violations. The financial resources derived from oil exports can potentially embolden rulers to act with impunity, raising ethical concerns about the use of petrodollars.

d) Peak Oil and Global Depletion: Experts highlight the unspoken factor of Peak Oil in the U.S. oil agenda. The quest for secure oil supplies and control over resources can influence foreign policy decisions, sometimes leading to military interventions.

e) Libya as a Case Study: Examining examples like Libya provides insights into the complex interplay of petrodollars, geopolitics, and international relations. Understanding the role of oil in shaping global dynamics is crucial for navigating the complexities of contemporary conflicts.

Thus, petrodollars wield considerable influence in global affairs, and their deployment can have far-reaching consequences. Whether fueling economic development or contributing to geopolitical tensions, the ethical and strategic considerations surrounding petrodollars remain central to discussions on war, oppression, and the broader dynamics of international relations.

Threat to the Petrodollar System

Saudi Arabia's potential shift to trading oil in Yuan, especially with China being its major oil consumer, poses a threat to the petrodollar system. The recent sanctions against Russian banks, limiting their access to the SWIFT system, exemplify the vulnerability of nations relying on the dollar. While Saudi Arabia has deep ties with the U.S., recent diplomatic tensions may push them to reconsider traditional allegiances. If Saudi Arabia embraces the Yuan for oil transactions, it could mark a significant move away from the dollar and challenge the existing global economic order. The rise of alternative currencies like the Renminbi could reshape the dynamics of global trade, impacting the strength of the U.S. dollar and requiring nations to adjust their currency reserves accordingly.

Negotiations between China and Saudi Arabia are signaling a potential shift away from the U.S. dollar as the global reserve currency. Saudi Arabia, a top oil producer, is considering pricing oil sales to China in Yuan instead of the petrodollar, marking a significant departure from the long-standing petrodollar system. China's increasing share of Saudi oil exports and its offers of lucrative incentives are contributing to this transformation. If successful, it could elevate the Yuan's standing and challenge the dominance of the U.S. dollar in global trade. The implications include potential economic challenges for the U.S., particularly if the dollar loses its reserve status. The situation is complicated by geopolitical tensions and the evolving global economic landscape, with China positioning itself as a major player in the Gulf region. The shift towards alternative currencies for oil transactions, such as the Yuan, introduces uncertainties and potential risks for the existing financial order.

How Deep Is Europe's Dependence on Russian Oil & Gas?

The United States faces challenges in supplying natural gas to Europe, given the surplus commitments to Mexico and Canada. With only a minimal surplus for the European Union (EU), the shift towards alternative energy sources and the reduction of reliance on Russian gas is hampered by contractual obligations. Experts estimate that the cost difference between liquefied natural gas (LNG) and piped gas for a 90-day consumption period could be $540 billion versus $86 billion, signaling potential economic strain for the EU. Russia's influence in the energy sector, coupled with its strategic decisions, such as accepting only rubles for natural gas from April 1, presents a financial war scenario with the West. European nations, heavily dependent on Russian gas, could face economic collapse if they sever ties with Russia. The German economy, a major player in the EU, is particularly vulnerable, prompting complex decisions in navigating geopolitical pressures. The EU's dependence on Russian gas, amounting to 45% of imports and 40% of consumption, underscores the challenges in reducing reliance on Russian energy. Despite discussions on diversification, Europe's declining gas production, stable demand, and insufficient alternative supplies contribute to persistent dependence on Russian gas. The possibility of disruptions in Russian gas supplies, exacerbated by the Ukraine crisis, has raised concerns about refilling gas storage and the overall impact on Europe's energy security.

Why the U.S. Can’t Quickly Wean Europe from Russian Gas

The Biden administration's efforts to increase natural gas exports to Europe face substantial challenges due to the limited availability of export and import terminals. The immediate options are constrained, leaving little choice but to appeal to Asian buyers for LNG tankers destined for Europe. Robert McNally, a former energy adviser to President George W. Bush, acknowledges the current limitations but envisions a future where the United States, with an expanded network of gas terminals, could play a pivotal role in helping Europe reduce its reliance on Russian gas. The complexity arises from the nature of natural gas, which requires an intricate process for transportation. Unlike crude oil, it cannot be easily shipped on oceangoing vessels. Instead, it undergoes a costly liquefaction process at export terminals, primarily located on the Gulf Coast. The liquefied gas is then loaded onto specialized tankers, and upon reaching its destination, the process is reversed to convert LNG back into its gaseous form. The construction of large-scale export or import terminals involves a significant financial investment, with costs exceeding $1 billion. Moreover, the lengthy processes of planning, obtaining permits, and completing construction extend the timeline for these projects. As of now, the United States has seven export terminals, while Europe boasts 28 large-scale import terminals that receive LNG from various suppliers, including Qatar and Egypt. The constraints on terminal infrastructure pose a hurdle to the immediate implementation of plans to bolster natural gas supplies to Europe, emphasizing the need for substantial investment and strategic planning to enhance energy security in the region.

Countries that depend on Russian Oil & Gas

Since Russia's invasion of Ukraine, the geopolitical and economic implications on the oil and gas sector have been profound. This article delves into the countries that heavily depend on Russian oil, the dynamics of global oil trade, and the evolving strategies that Russia is employing to assert its dominance.

Top Crude Oil Exporters (2019):

Ø Saudi Arabia ($145bn)

Ø Russia ($123bn)

Ø Iraq ($73.8bn)

Ø Canada ($67.8bn)

Ø US ($61.9bn)

Countries Dependent on Russian Oil:

Ø China (27.3%)

Ø Netherlands (16.5%)

Ø Germany (6.91%)

Ø South Korea (5.98%)

Ø Belarus (5.29%)

Ø Poland (5.06%)

Ø Italy (4.83%)

Ø Finland (3.59%)

Ø Turkey (2.99%)

Ø Japan (2.64%)

Ø US (1.82%)

Ø India (0.9%)

OPEC and Global Oil Production:

Ø OPEC (13 member nations) produces 40% of the world's crude oil.

Ø Top five oil-producing countries: US, Russia, Canada, China.

Top Five Consumers of Crude Oil:

Ø US (20.54 mbpd)

Ø China (14.01 mbpd)

Ø India (4.92 mbpd)

Ø Japan (3.74 mbpd)

Ø Russia (3.70 mbpd)

Russia's Weaponisation of Gas Trade:

Ø Russia demands "unfriendly" nations pay in gold or ruble for gas.

Ø This move strengthens Russia's currency and deepens its gold reserve.

Potential Shift to Petro Yuan:

Ø China and Saudi Arabia in talks to price oil contracts in Yuan.

Ø Ongoing talks for almost a decade, not triggered by the Ukraine crisis.

US Gas Sales to Europe:

Ø US sells 69% surplus to Mexico and 30% surplus to Canada, limiting availability for EU.

Ø EU heavily depends on Russia for gas, with significant economic consequences if delinked.

Thus, the global oil and gas landscape is intricately woven with geopolitical considerations, economic dependencies, and evolving strategies. Russia's influence on oil prices, coupled with its maneuvers in the gas trade, has significant implications for both regional and global economies. As the world grapples with these complexities, the need for diversified and resilient energy strategies becomes increasingly apparent.

Putin's War and World Energy

Throughout history, the United States has consistently aimed to prevent closer cooperation between Germany and Russia. Despite historical tensions between Germany and Russia, both being major European powers, economic ties have existed. The U.S. policy seeks to impede this connection, rooted in the Cold War era when the Soviet Union supported pacifist movements in Germany during the 1980s. The underlying concern is that a stronger Germany-Russia alliance could challenge American nuclear strategy, especially considering the potential impact on European interests in the event of a nuclear war.

Russia Is A Major Supplier Of Oil To The U.S.

Russia plays a notable role as a major supplier of oil to the United States. In 2021, Russia produced 10.1 million barrels per day (BPD), securing the second position after the U.S. at 11.3 million BPD, with Saudi Arabia following closely at 9.3 million BPD. Despite being a leading producer, the U.S. consumes substantially more oil (17.2 million BPD) than both Russia (3.2 million BPD) and Saudi Arabia (3.5 million BPD) combined. The crucial point is that the U.S. is a net importer of crude oil, while Russia and Saudi Arabia are significant exporters. This distinction renders the U.S. more susceptible to oil price fluctuations, while higher oil prices act as a net advantage for Russia and Saudi Arabia. Russia's contribution of 7% to U.S. oil imports in late 2021 emphasizes its impact, and finding alternative sources may exert additional upward pressure on global oil prices.

How & Why Petrodollar is ending?

The petrodollar's stability is waning due to various geopolitical events, including American military actions in the Middle East. The narrative proposes that actions taken by the U.S., particularly in Iraq, Egypt, Libya, and Syria, are connected to the 1973 petrodollar deal with Saudi Arabia. It implies that Saudi Arabia, a key player in the petrodollar system, is taking strategic measures such as influencing oil prices and aligning with the U.S. to defend its market share and exert dominance. The theory explores the possibility that the recent decline in oil prices, orchestrated by OPEC nations led by Saudi Arabia, is impacting the U.S. energy sector. It raises questions about Saudi Arabia's motives, whether to hinder U.S. energy independence, collaborate with the U.S. against common adversaries like Russia and Iran, or facilitate arms deals with China. Thus, the petrodollar's stability is under strain due to changing geopolitical dynamics, and the dominance of a single currency and country controlling global oil costs may be facing challenges.

Countries bypassing the Petrodollar

There has been significant shift in international transactions, with countries increasingly bypassing the use of the U.S. dollar and opting for payments in their domestic currencies. Several key developments contribute to this trend:

a) Russia-China Energy Deal: Russia and China signed a substantial $400 billion energy deal, solidifying a critical relationship based on Russia's resource abundance and China's low-cost labor and manufacturing capabilities.

b) BRICS Nations Bypassing Dollar: The BRICS nations—Brazil, Russia, India, China, and South Africa—have taken steps to bypass the U.S. dollar, establishing the New Development Bank as an alternative to the Western-backed IMF.

c) Anti-Dollar Alliance in the Eastern Hemisphere: An anti-dollar alliance is emerging in the Eastern hemisphere as nations resist potential hindrances to their growth from American imperialism.

d) SWIFT System Alternatives: Around 23 countries, including U.S. allies such as Germany, France, and the UK, are setting up swap lines that circumvent the dollar and the SWIFT payment system, signaling a diversification in global transactions.

e) Serious Threat to Petrodollar:

Ø The collective decision by China, Russia, India, Iran, Venezuela, Saudi Arabia, and the UAE to conduct oil and gas transactions in mutual currencies poses a serious challenge to the petrodollar system.

Ø Russia's conditions for supplying gas and oil only in Rubles, linked to gold, and the potential disruption of pipelines to Europe underscore the threat to the traditional petrodollar structure.

Ø The strategic partnership between Russia and China, evident in their silent approval and cooperation, further emphasizes the shift away from the U.S. dollar.

Ø The analysis suggests that a fracture in the world's monetary system into competing East/West structures is imminent, marking the end of the 50-year global petrodollar system initiated by Putin's actions.

Thus, a geopolitical and economic landscape where countries are actively seeking alternatives to the U.S. dollar, challenging the long-standing dominance of the petrodollar system.

Is the 50 years of petrodollar coming to an end?

The 50-year era of the petrodollar is facing potential disruption, marked by recent diplomatic optics and changing dynamics. Secretary of State Blinker’s visit to the Saudi crown prince in a tent, rather than the palace, symbolizes a shift in the relationship dynamics, highlighting diminished reliance on Saudi Arabia compared to the 1970s.

The petrodollar system originated during the Yom Kippur war in 1973 when the US, facing economic challenges and an oil embargo, struck a deal with Saudi Arabia. This arrangement has favored the Middle East more than the US, pouring wealth into Gulf States, Iraq, and Iran. However, major changes are underway. Russia, a key player in the BRICS alliance, has announced upcoming transformations in cross-border transactions, signaling a shift in the global economic order. China and Russia, now closely collaborating with Saudi Arabia and Gulf countries, are challenging the traditional petrodollar alliance. As the US watches these changes unfold, tensions are rising, especially with oil prices becoming shaky. The US, back at peak oil production, may not want prices to surge, causing irritation in Saudi Arabia. This has the potential to lead to an oil price war, with Saudi Arabia possibly lowering oil prices to render shale production unprofitable—a move echoing past strategies. This geopolitical and economic landscape contributes to the uncertainty surrounding the future of the petrodollar.

Death of Petro Dollar? How & Why?

Putin's invasion of Ukraine on February 24, 2022, marked not just a military move but also symbolized the official end of the petrodollar system. Russia, alongside China, had been preparing for this moment for years. Anticipating SWIFT system exclusions and sanctions from the West, Russia strategically shut off oil and gas pipelines to Europe, causing massive disruptions in price and supply and challenging the Western monetary system. The move aimed to re-monetize gold and exit SWIFT system abuses, achieving this through the invasion of Ukraine. With the West unintentionally freeing Russia from SWIFT, Russia declared that Russian oil and Ukrainian wheat must be paid for in gold or using the ruble-Yuan gold-backed payment system. This leverage, as a major oil producer, caused immediate shocks to the Western world, impacting both heating homes and disrupting wheat production.

China's silence and lack of condemnation indicated approval and cooperation. China stepped in to absorb Russian production of oil and wheat, utilizing the Yuan-Ruble facility and, at some point, overtly stating gold backing of the system. This led to a clear fracture in the world's monetary system, establishing two competing East/West structures and officially ending the 50-year global petrodollar system by Putin.

The threat to the petrodollar mirrors historical challenges by figures like Charles De Gaulle or Gaddafi but on a larger scale. Putin's position, compared to leaders like Saddam and Gaddafi, may prove more resilient in challenging the fraudulent petrodollar monetary system. Additionally, Saudi Arabia's consideration of selling oil in Chinese Yuan rather than US dollars adds another layer to the discussion, highlighting the potential shift in the world's economic landscape if the petro Yuan becomes the preferred currency for oil transactions.

What Comes Next?

A historical sequence of events unfolded: Countries, requiring oil for their economies, exported goods to the United States in exchange for dollars. These dollars were then used to acquire oil from Saudi Arabia. To add a twist, OPEC nations invested their dollar profits back into America's bond market, yielding a cycle where the US, while running trade deficits, enjoyed lowered borrowing costs and increased funds for purchasing American debt. This intricate system allowed the US to navigate trade imbalances and government financing without immediate financial repercussions. As the Petrodollar era fades, the quest for a new global financial framework is underway, with digital currencies and innovative economic models at the forefront of potential replacements.

As fossil fuels lose their appeal and the global shift to renewable energy gains momentum, the influence of oil on the world economy is gradually waning. Simultaneously, the decline of the USD prompts a search for alternative currencies for international transactions. In this evolving landscape, digital currencies and the concept of digital scarcity emerge as crucial elements in addressing challenges posed by the existing fiat-currency paradigm. The demise of the Petrodollar is evident, raising the question of what will fill its void. One plausible scenario is that the US could sustain its significant trade deficits, a trend persisting since 1975, without concerns about a decline in demand for the dollar.

De-Dollarization in a multi polar world: De-dollarization refers to the process by which a country or a group of countries reduces their reliance on the U.S. dollar in their international trade and financial transactions. This phenomenon is often discussed in the context of a multipolar world, where power is distributed among multiple major economies rather than being dominated by a single superpower. Key elements of De-dollarization: Motivations for De-Dollarization, Currency Agreements and Bilateral & Barter Trade, International Monetary System Reforms, Use of Alternative Currencies, Development of Regional Financial Institutions, Gold and Digital Currencies (including Bitcoin) etc.

Is Ukraine war signifies End of Petrodollar

Vladimir Putin's invasion of Ukraine on 24th February, 2022 not only marked a geopolitical conflict but also signaled the official end of the petrodollar system. Do you still think that President Putin acted in haste with Ukraine offensive? This move, carefully strategized by Russia and China over the years, is reshaping the world's economic dynamics:

NATO Expansion and Red Lines:

· Russia had set red lines, particularly opposing NATO expansion into Ukraine.

· Anticipating SWIFT system exclusions and massive sanctions, Russia prepared for potential consequences.

Oil and Gas Leverage:

· Russia, possessing significant Yuan, gold, and commodity reserves, could disrupt oil and gas pipelines to Europe.

· This disruption could lead to substantial price and supply shocks, impacting Western markets and the monetary system.

Monetizing Gold and Exiting SWIFT:

· Russia and China sought ways to re-monetize gold and exit SWIFT's geopolitical influence.

· The invasion provided a pretext for Russia to declare itself a SWIFT system outcast, demanding alternative payment methods.

Gold-Backed Payments and Yuan-Ruble Facility:

· Russia might demand payment for oil and wheat in gold or through a ruble-Yuan gold-backed payment system.

· China, remaining silent, is likely to cooperate with Russia, absorbing its oil and wheat production via the Yuan-Ruble facility.

World Monetary System Fracture:

· The West would likely label these moves as acts of global aggression, leading to a clear fracture in the world's monetary system.

· The global petrodollar system, in place for 50 years, is effectively ended by Putin.

SPFS and Dollarization:

· Russia's SPFS, an equivalent to SWIFT, and China's CIPS could integrate with Bharat's SFMS.

· The impact of massive dollarization, if Russia is removed from SWIFT, would be significant, weakening the US dollar.

Competing Currency Transactional System:

· A new system by Russia, China, and Bharat could compete against SWIFT, challenging the dominance of the US dollar.

· This shift may lead to a new economic alliance with countries like those in Africa and Saudi Arabia.

Eurasian Union and Global Economic Shift:

· The emergence of an alternate digital economic system and a global digital currency is anticipated.

· Developed countries may witness a significant decline in their share of the world's income.

Impact on US Economy:

· Removing countries from SWIFT could adversely affect the US economy, given the dollar's role as a global reserve currency.

· The US, with a staggering debt of $34 trillion, could face higher transaction costs and interest rates.

In this evolving scenario, calls to eject countries from SWIFT should be carefully considered, recognizing the potential repercussions on the global economic order and the complex interplay of geopolitical and economic forces.

Conclusion:

The demise of the petrodollar could usher in a transformative era, disrupting the current dynamic. Commodity-exporting nations might break free from the dollar, opting to peg their currencies to a basket of commodities. Importing countries would need these currencies to settle payments for energy and agricultural imports, leading to appreciating currencies in commodity-exporting regions due to supply deficits. This shift could mark the beginning of a multipolar world with bilateral trade agreements replacing the petrodollar-centered order. Regions heavily reliant on raw material imports, such as Europe and Japan, may face challenges, while countries like Russia, India, and China could strengthen economic and geopolitical ties through bilateral agreements. The impact on the United States might be less severe due to its domestic-focused economy and potential self-sufficiency in raw materials. However, the decline of the petrodollar could still result in increased inflation and interest rates.

CA Harshad Shah, Mumbai harshadshah1953@yahoo.com

Another important thing to understand was the end of the Bretton Woods Agreement and Nixon taking the US off the gold standard.

What the F#%^ Happened in 1971? The Dramatic Acceleration of our Current Economic Collapse…

Nixon Takes Us off The Gold Standard and Dollar Debasement and Economic Collapse Begins

The charts and graphs below from WTF Happened in 1971 are some of the most fascinating I have ever seen. What is most interesting is that the site owner failed to “Lead with the Punchline” and didn’t explain What the F%#$ Happened in 1971.

The short answer is that President Nixon took the country off the final vestiges of the gold standard, creating the widespread economic and societal decline that you see represented in the charts and graphs.

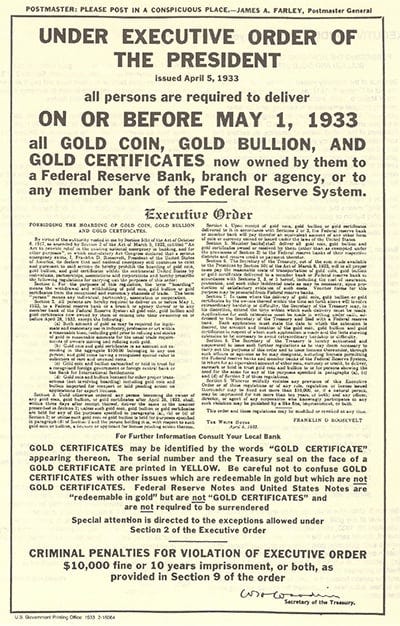

The beginning of debasement started with communist Presidents Woodrow Wilson, who passed the Federal Reserve Act in 1913 and Franklin Delano Roosevelt when he confiscated the people’s gold under “executive order” in 1933, but foreign governments could still purchase and redeem US Government Bonds in physical gold up until 1971….